Some risks are binary while others are not. Binary risks are ones in which a situation really only has two outcomes, success or failure. For example, entitlement risk is often a binary risk in a development project. The risk of defaulting on your loan is another potential binary risk. Non-binary risks have less teeth, if you will, and don’t necessarily drastically alter the performance of an investment. A good example of a non-binary risk would be vacancy being 20% higher than projected (8.4% instead of 7%). While definitely painful, this type of non-binary risk is not enough to blow up a deal.

While investors are typically concerned with non-binary risks because they are looking to achieve the highest return possible, investors should also pay close attention to binary risks or multiple non-binary risks turning into a loss of capital, rather than focusing solely on underperformance.

I believe the most important binary risk in multifamily investing is refinance risk, or “refinancability”. Refinance risk is the risk of not being able to refinance your debt upon maturity and thus being forced to sell which is likely to be in a time of adverse market conditions. Refinance risk is exacerbated by higher going-in leverage, interest-only payments, shorter maturities, underperformance by the property, and adverse capital markets conditions (widening spreads, rising index rates, lower valuations). This list of risks may sound like a call for long-term, fixed rate, amortizing, low leverage debt, and it is, except for the fact that high returns and reposition opportunities are rarely found in buying stabilized property (above 90% occupancy) which would qualify for agency debt. Furthermore, long-term debt hinders your ability to exit a deal quickly, which opens the investment up to market risks for longer periods of time. Since the future is less predictable than the near term, market risk increases with the length of the investment horizon.

Even more important is the incompatibility of reposition projects and permanent financing. Generally speaking, properties with less than 90% occupancy cannot be financed by GSEs or CMBS lenders. Given the liquidity of the market, most apartment owners who are capable of maintaining 90% occupancy are equally capable of either 1) implementing a value-add or reposition business plan on their own asset or 2) market their property for sale at a price based on value-added pro forma (sellers will sell value-add properties at a price which will yield core to core-plus returns). Therefore, finding an appropriately priced, true value-add opportunity with above 90% occupancy is nearly impossible. With this understanding, we actively look for deals with sub-90% occupancy which exhibit idiosyncratic distress located in an otherwise well-performing sub-market (this is also extremely difficult to find, given the aforementioned liquidity of the market).

Another issue with permanent financing for value-add business plans is it typically doesn’t offer an efficient capitalization of capex dollars. More specifically, bridge loans allow investors to draw down renovation funds from a lender’s capex reserve as needed instead of needing to raise the full capex budget out of equity, which is far more expensive.

However, the downsides of bridge loans are the higher leverage point, higher interest costs, and shorter maturities. We can control how much proceeds we take from a lender and push for longer durations but have little influence over their pricing. This means we can focus on buying at the right price, ensuring a significant value-add opportunity exists, and the going-in leverage point is conservative. The best way we can ensure bridge loan success is by analyzing the “refinancability” of our proposed bridge loan strategy for any given acquisition.

I recently updated our underwriting model to include a handful of two-way table sensitivity analyses as well as a unique “refinancability” table. The refinancibility table allows us to stress test the projected leverage for a deal and see what a refinance would look like in any given month (thanks to Hlookup). I’m also able to perform operational and capital markets shocks to the model to see the effect on the new loan’s proceeds and DSCR based on adverse assumptions. If you would like to try this out for yourself, you can download our updated model here and click on the Sensitivities tab and toggle the refinance assumptions in column Y.

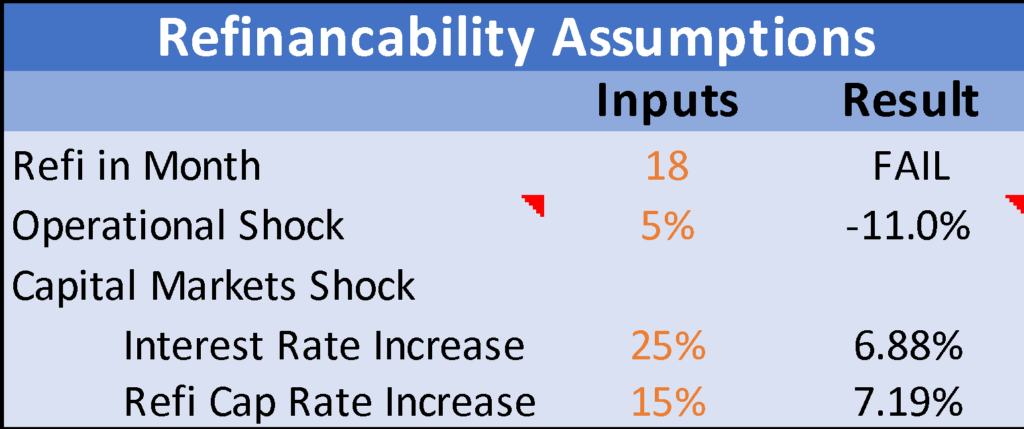

Here is an example, testing out our new refinancability test (these are numbers based loosely on a live deal we recently underwrote).

P.S. The price I’m assuming in the model is 15% lower than the ask price… So really this deal makes no sense.

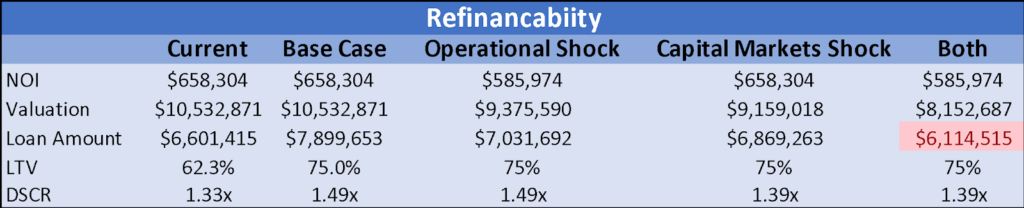

As you can see, the current column shows the projected NOI in the specified refi month (18 months into the investment). The current column uses the refinance cap rate assumption on the Inputs tab to calculate the base case valuation which is then used to calculate the projected refinance loan amount for the base case. The table above shows that the current bridge loan balance at $6.6MM can easily be refinanced by a new permanent loan of $7.9MM based on base case assumptions.

Next come the stress tests. An operational shock, in this case, is 5% lower revenue than base case assumptions, which results in an 11% reduction in projected NOI at month 18. This means the new loan will be based on this lower NOI and base case cap rate and interest rate assumptions. The projected valuation in the operational shock scenario is more than $1MM lower than the base case which means the new loan is only $7MM. However, this loan is still enough proceeds to takeout the existing bridge loan and avoid taking on a second bridge loan or being forced to sell. The next scenario is a capital markets shock. This scenario holds the base case operating assumptions stable but increase both the refinance cap rate as well as the interest rate for the new loan. The refinance cap rate affects the value the lender is willing to place on the asset while the higher interest rate will hurt the DSCR, making the max proceeds subject to a minimum coverage ratio lower. In the above example, the refinance cap rate is widened by 15% to 7.19% and the interest rate is increased by 25% to 6.88%. The result of this capital markets shock is a significant reduction in proceeds but still enough to refinance the existing loan. Also, the operational shock and capital markets shock both project refinances with healthy DSCRs so potentially the proceeds could be pushed higher.

Lastly, the both column projects a refinance in month 18 which includes both an operational shock (11% decline in NOI off pro forma) as well as the aforementioned capital markets shock (15% increase in cap rate and 25% increase in interest rate). As you can see, the projected refinance proceeds are less than the outstanding balance on the bridge loan ($6.1MM projected refinance versus $6.6MM existing loan). If you wanted to lower the investment’s refinance risk and pass the “both” scenario, you could lower the bridge loan’s proceeds to $6MM. This tool can be helpful in identifying risks in the business plan and potentially mitigating them.

In conclusion, even though it is late cycle and valuations are high, we are still pursuing bridge financing for our acquisitions because we believe we can find risk-adjusted opportunities which warrant bridge loan execution. Some worry about interest rates rising but the tightening cycle seems to have concluded and the market is pricing rate cuts over rate hikes in the coming year. Additionally, it is highly unlikely to find a deep value-add/opportunistic type of opportunity which is 90%+ occupied (essentially precluding those opportunities from permanent financing). This is because most owners operating property at 90%+ occupancy are well-capitalized and are either going to sell at a price based on pro forma (future valuation, post-renovation) or will implement the value-add business plan themselves. Furthermore, I think the high level of real estate capital market liquidity, especially for multifamily, will likely mitigate any prolonged periods of capital market dislocation, thus creating a higher likelihood of being able to refinance successfully. This is especially true, given the diversity of available debt capital for multifamily (GSEs, HUD, banks, life insurance companies, debt funds, private debt). All we can do is wait for the turn of the cycle to see what happens.